របាយការណ៍នេះនឹងផ្តល់នូវការវិភាគអំពីកត្តាចម្បងដែលជះឥទ្ធិពលលើតម្លៃមាស ទៅកាន់វិនិយោគិន។

ការបដិសេធ (Disclaimer): ព័ត៌មានទាំងអស់ដែលបង្ហាញគឺសម្រាប់ក្នុងគោលបំណងអប់រំតែប៉ុណ្ណោះ ហើយមិនគួរត្រូវប្រើប្រាស់ជាដំបូន្មានហិរញ្ញវត្ថុ ឬការណែនាំសម្រាប់ការសម្រេចចិត្តលើការជួញដូរ ឬការវិនិយោគនោះទេ។

ការវិភាគបែបសេដ្ឋកិច្ច (Fundamental Analysis)

ការសង្ខេបស្ថានភាពសេដ្ឋកិច្ចពីមុន៖ នៅក្នុងខែឧសភា ឆ្នាំ២០២៦ ទីផ្សារហិរញ្ញវត្ថុសកលបានដំណើរការក្នុងបរិយាកាសម៉ាក្រូសេដ្ឋកិច្ចចម្រុះ ដែលកំណើនសេដ្ឋកិច្ចនៅតែបង្ហាញភាពធន់ ប៉ុន្តែមិនទាន់មានសន្ទុះច្បាស់លាស់។ ទោះបីជាការព្រួយបារម្ភអំពីវិបត្តិសេដ្ឋកិច្ច (Recession) មិនបានកើនឡើងក៏ដោយ ក៏ភាពមិនប្រាកដប្រជានៅតែបន្តមាន ខណៈវិនិយោគិនបន្តវាយតម្លៃឡើងវិញអំពីពេលវេលា និងទិសដៅនៃការផ្លាស់ប្តូរគោលនយោបាយរូបិយវត្ថុ ស្របពេលដែលអតិផរណានៅតាមបណ្តាប្រទេសសេដ្ឋកិច្ចធំៗមានការថយចុះមិនស្មើគ្នា។

នៅសហរដ្ឋអាមេរិក សកម្មភាពសេដ្ឋកិច្ចនៅតែមានស្ថិរភាព ដោយមានការគាំទ្រពីតម្រូវការប្រើប្រាស់របស់ប្រជាពលរដ្ឋ និងទីផ្សារការងារដែលនៅតែមានភាពរឹងមាំ។ ទោះជាយ៉ាងណា អតិផរណានៅតែបង្ហាញសញ្ញានៃការបន្តស្ថិតក្នុងកម្រិតខ្ពស់ ជាពិសេសក្នុងវិស័យសេវាកម្ម ដែលធ្វើឱ្យធនាគារកណ្តាលអាមេរិក (Federal Reserve) បន្តប្រុងប្រយ័ត្ន។ ជាលទ្ធផល ការរំពឹងទុកអំពីការកាត់បន្ថយអត្រាការប្រាក់ក្នុងរយៈពេលខ្លីត្រូវបានពន្យារពេលជាបន្តបន្ទាប់ ដែលធ្វើឱ្យទីផ្សារពឹងផ្អែកកាន់តែខ្លាំងលើទិន្នន័យសេដ្ឋកិច្ចដែលចេញផ្សាយ។

អត្រាផលទុនលើមូលបត្របំណុលរដ្ឋាភិបាលអាមេរិក (US Treasury Yields) នៅតែស្ថិតក្នុងកម្រិតខ្ពស់ និងមានភាពប្រែប្រួលពេញមួយខែ ដោយឆ្លុះបញ្ចាំងពីក្តីបារម្ភជុំវិញអតិផរណាដែលនៅតែជាប់ខ្ពស់ ភាពមិនច្បាស់លាស់ផ្នែកហិរញ្ញវត្ថុសាធារណៈ និងការផ្លាស់ប្តូរការរំពឹងទុកអត្រាការប្រាក់ ជាជាងការរំពឹងទុកពីការកើនឡើងខ្លាំងនៃកំណើនសេដ្ឋកិច្ច។ បរិបទនេះបានធ្វើឱ្យលក្ខខណ្ឌហិរញ្ញវត្ថុនៅតែតឹងរ៉ឹង និងកំណត់ការកើនឡើងនៃចំណង់ទទួលហានិភ័យរបស់វិនិយោគិន។

ក្រៅពីសហរដ្ឋអាមេរិក អឺរ៉ុបនៅតែបង្ហាញកំណើនសេដ្ឋកិច្ចទន់ខ្សោយ ដោយសកម្មភាពឧស្សាហកម្មទាបបានដាក់សម្ពាធលើទស្សនៈទីផ្សារ ទោះបីមានសញ្ញាស្ថិរភាពខ្លះនៅក្នុងវិស័យសេវាកម្មក៏ដោយ។ ចិនបានបន្តដំណើរការស្ដារសេដ្ឋកិច្ចឡើងវិញជាបណ្តើរៗ ដោយមានការគាំទ្រពីវិធានការគោលនយោបាយជាក់លាក់ ប៉ុន្តែល្បឿននៃការងើបឡើងវិញនៅតែមិនស្មើគ្នា និងទាបជាងការរំពឹងទុកពីមុន។

ជារួម លក្ខខណ្ឌម៉ាក្រូសេដ្ឋកិច្ចសកលនៅតែស្ថិតក្នុងដំណាក់កាល “រង់ចាំមើល” (Wait-and-See) ខណៈទីផ្សារមានភាពប្រតិកម្មខ្លាំងចំពោះទិន្នន័យអតិផរណា សេចក្តីថ្លែងការណ៍របស់ធនាគារកណ្តាល និងការវិវត្តន៍ភូមិសាស្ត្រនយោបាយ។ ក្នុងបរិបទនេះ តម្លៃមាសនៅតែទទួលបានការគាំទ្រ ដោយវិនិយោគិនបន្តប្រើប្រាស់មាសជាឧបករណ៍ការពារហានិភ័យពីភាពមិនច្បាស់លាស់នៃគោលនយោបាយ អតិផរណាដែលនៅតែខ្ពស់ និងហានិភ័យម៉ាក្រូសេដ្ឋកិច្ចផ្សេងៗ។ ទោះបីអត្រាការប្រាក់ពិតប្រាកដ (Real Yields) ស្ថិតក្នុងកម្រិតខ្ពស់នៅពេលខ្លះក៏ដោយ មាសនៅតែរក្សាបាននូវភាពរឹងមាំ ដោយបញ្ជាក់ពីតួនាទីរបស់វាជាទ្រព្យសុវត្ថិភាព (Safe-Haven Asset) ក្នុងបរិយាកាសសេដ្ឋកិច្ចមិនប្រាកដប្រជា។

ការសម្រេចអត្រាការប្រាក់របស់ធនាគារកណ្តាលអាមេរិកនៅសប្តាហ៍ក្រោយ

តើកត្តាអ្វីខ្លះគួរត្រូវបានពិចារណាមុនការសម្រេចអត្រាការប្រាក់របស់សហរដ្ឋអាមេរិកនៅសប្តាហ៍ក្រោយ?

ទីផ្សារការងារ់៖ ទីផ្សារការងាររបស់សហរដ្ឋអាមេរិកនៅតែបង្ហាញភាពធន់ ដូចដែលបានឆ្លុះបញ្ចាំងតាមរយៈទិន្នន័យការងារចុងក្រោយ។ ចំនួនការងារថ្មីក្រៅវិស័យកសិកម្ម (Nonfarm Payrolls – NFP) នៅតែបង្ហាញកំណើនលើសការរំពឹងទុករបស់ទីផ្សារ ខណៈអត្រាគ្មានការងារធ្វើ (Unemployment Rate) នៅតែមានស្ថិរភាព។ ទន្ទឹមនឹងនេះ ប្រាក់ឈ្នួលជាមធ្យមក្នុងមួយម៉ោង (Average Hourly Earnings) ក៏បន្តបង្ហាញកំណើនថេរ ដែលបង្ហាញថាស្ថានភាពមូលដ្ឋាននៃទីផ្សារការងារនៅតែមានសុខភាពល្អ ទោះបីមានសញ្ញានៃការថមថយបន្តិចបន្តួចបើប្រៀបធៀបទៅនឹងឆ្នាំមុនៗក៏ដោយ។

ភាពរឹងមាំនៃទីផ្សារការងារផ្តល់ភាពបត់បែនកាន់តែច្រើនដល់ធនាគារកណ្តាលអាមេរិកក្នុងការរក្សាជំហរគោលនយោបាយបច្ចុប្បន្ន ខណៈអ្នករៀបចំគោលនយោបាយនៅតែផ្តោតលើការធានាឱ្យអតិផរណាត្រឡប់ទៅកាន់គោលដៅរយៈពេលវែងរបស់ខ្លួន។

អតិផរណា៖ ដោយសារស្ថានភាពទីផ្សារការងារនៅតែមានស្ថិរភាព អតិផរណាទំនងជាកត្តាសំខាន់បំផុតដែលនឹងមានឥទ្ធិពលលើការសម្រេចអត្រាការប្រាក់របស់ធនាគារកណ្តាលអាមេរិក។ ទិន្នន័យ CPI និង PPI ដែលនឹងត្រូវចេញផ្សាយនាពេលខាងមុខ នឹងផ្តល់ការយល់ដឹងបន្ថែមអំពីសម្ពាធតម្លៃបច្ចុប្បន្ន និងថាតើអតិផរណាកំពុងបន្តថយចុះឆ្ពោះទៅរកគោលដៅ 2% របស់ធនាគារកណ្តាលអាមេរិកដែរឬទេ។

សេណារីយ៉ូដែលទំនងបំផុតគឺ អតិផរណានឹងនៅតែស្ថិតក្នុងកម្រិតខ្ពស់មធ្យម ប៉ុន្តែជាទូទៅស្របតាមការរំពឹងទុករបស់ទីផ្សារ។ ប្រសិនបើរឿងនេះកើតឡើងធនាគារកណ្តាលអាមេរិក ត្រូវបានរំពឹងថានឹងរក្សាអត្រាការប្រាក់ឱ្យនៅដដែល ខណៈបន្តអនុវត្តវិធីសាស្ត្រដែលផ្អែកលើទិន្នន័យនៅក្នុងកិច្ចប្រជុំ Federal Open Market Committee (FOMC) លើកក្រោយ។ លទ្ធផលបែបនេះនឹងពង្រឹងការរំពឹងទុកថា អត្រាការប្រាក់អាចនៅក្នុងកម្រិតខ្ពស់រយៈពេលយូរជាងមុន ជាជាងបង្ហាញពីការបន្ធូរបន្ថយគោលនយោបាយរូបិយវត្ថុភ្លាមៗ។

កិច្ចប្រជុំនាពេលខាងមុខនេះក៏ជាកិច្ចប្រជុំ FOMC លើកដំបូងដែលដឹកនាំដោយលោក Kevin Warsh បន្ទាប់ពីការតែងតាំងជាប្រធានធនាគារកណ្តាលអាមេរិកកាលពីខែឧសភា ឆ្នាំ២០២៦។ ទោះបីការសម្រេចគោលនយោបាយរូបិយវត្ថុនៅតែផ្អែកលើទិន្នន័យសេដ្ឋកិច្ចក៏ដោយ វិនិយោគិននឹងតាមដានយ៉ាងយកចិត្តទុកដាក់លើសេចក្តីថ្លែងការណ៍គោលនយោបាយ ការព្យាករណ៍សេដ្ឋកិច្ច និងសន្និសីទសារព័ត៌មាន ដើម្បីស្វែងរកសញ្ញាអំពីរបៀបដែលថ្នាក់ដឹកនាំថ្មីអាចដោះស្រាយបញ្ហាអតិផរណា អត្រាការប្រាក់ និងទិសដៅគោលនយោបាយនាពេលអនាគត។

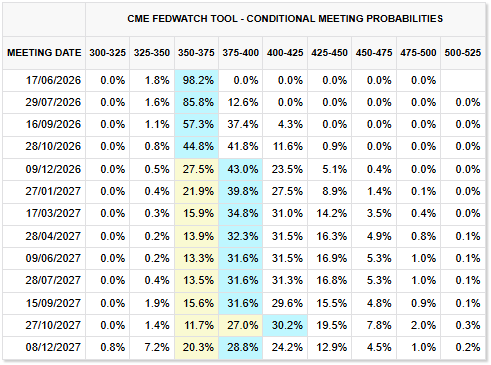

យោងតាមការកំណត់តម្លៃទីផ្សារបច្ចុប្បន្នដែលបង្ហាញដោយឧបករណ៍ CME FedWatch Tool វិនិយោគិនជាទូទៅរំពឹងថាធនាគារកណ្តាលអាមេរិកនឹងរក្សាអត្រាការប្រាក់បច្ចុប្បន្នក្នុងរយៈពេលខ្លី ដោយការសម្រេចចិត្តនាពេលអនាគតនឹងពឹងផ្អែកយ៉ាងខ្លាំងលើទិន្នន័យអតិផរណា និងទីផ្សារការងារដែលនឹងចេញផ្សាយបន្តទៀត។

សម្រាប់មាស បរិយាកាសអត្រាការប្រាក់ខ្ពស់ដែលអូសបន្លាយអាចកំណត់សន្ទុះកើនឡើងរបស់តម្លៃមាស តាមរយៈការគាំទ្រអត្រាផលទុនមូលបត្របំណុលរដ្ឋាភិបាលអាមេរិក និងប្រាក់ដុល្លារអាមេរិក។ ទោះជាយ៉ាងណា ហានិភ័យភូមិសាស្ត្រនយោបាយ ភាពមិនច្បាស់លាស់ផ្នែកហិរញ្ញវត្ថុសាធារណៈ និងតម្រូវការទ្រព្យសុវត្ថិភាព (Safe-Haven Asset) អាចបន្តផ្តល់ការគាំទ្រដល់មាស ដែលបង្ហាញថាទិសដៅរបស់មាសនឹងនៅតែពាក់ព័ន្ធយ៉ាងជិតស្និទ្ធជាមួយការវិវត្តន៍អតិផរណា និងទស្សនៈទីផ្សារទូទៅ។

ភាពតានតឹងភូមិសាស្ត្រនយោបាយ

សង្គ្រាមពាណិជ្ជកម្មរវាងសហរដ្ឋអាមេរិក និងចិនោ៖ ប្រធានាធិបតីសហរដ្ឋអាមេរិក លោក Donald Trump បានជួបជាមួយប្រធានាធិបតីចិន លោក Xi Jinping ក្នុងកិច្ចប្រជុំកំពូលសហរដ្ឋអាមេរិក-ចិន ចាប់ពីថ្ងៃទី១៣ ដល់ថ្ងៃទី១៥ ខែឧសភា។ កិច្ចពិភាក្សាបានផ្តោតជាចម្បងលើពាណិជ្ជកម្ម ការវិនិយោគ និងកិច្ចសហប្រតិបត្តិការសេដ្ឋកិច្ចទូលំទូលាយរវាងសេដ្ឋកិច្ចធំបំផុតទាំងពីររបស់ពិភពលោក។

ទោះបីមិនមានកិច្ចព្រមព្រៀងសំខាន់ណាមួយត្រូវបានប្រកាសក៏ដោយ ភាគីទាំងពីរបានយល់ព្រមពង្រីកកិច្ចសន្ទនាតាមរយៈយន្តការថ្មីៗសម្រាប់កិច្ចសហប្រតិបត្តិការផ្នែកពាណិជ្ជកម្ម និងការវិនិយោគ ព្រមទាំងបង្ហាញឆន្ទៈក្នុងការកាត់បន្ថយរបាំងពាណិជ្ជកម្មមួយចំនួន។ វឌ្ឍនភាពក៏ត្រូវបានរាយការណ៍ក្នុងវិស័យពាណិជ្ជកម្មកសិកម្ម ការទិញយន្តហោះ និងការពិភាក្សាអំពីការកាត់បន្ថយពន្ធគយទៅវិញទៅមកផងដែរ។ ជារួម កិច្ចប្រជុំកំពូលនេះបានជួយលើកកម្ពស់ទស្សនៈវិជ្ជមានរបស់ទីផ្សារ ដោយកាត់បន្ថយក្តីបារម្ភអំពីការកើនឡើងបន្ថែមទៀតនៃភាពតានតឹងពាណិជ្ជកម្មរវាងសហរដ្ឋអាមេរិក និងចិន។ វិនិយោគិននឹងបន្តតាមដានការវិវត្តន៍បន្ថែម ខណៈលោក Xi ត្រូវបានរំពឹងថានឹងធ្វើទស្សនកិច្ចនៅសេតវិមាននៅចុងឆ្នាំនេះសម្រាប់កិច្ចប្រជុំបន្ត។

ជម្លោះរវាងសហរដ្ឋអាមេរិក និងអ៊ីរ៉ង់ និងការវិវត្តន៍នៅមជ្ឈិមបូព៌ា៖ ខែឧសភាបានឃើញការវិវត្តន៍ជាបន្តបន្ទាប់ជុំវិញជម្លោះរវាងសហរដ្ឋអាមេរិក និងអ៊ីរ៉ង់។ មានសេចក្តីរាយការណ៍ថា ភាគីទាំងពីរកំពុងពិភាក្សាអំពីអនុស្សរណៈនៃការយោគយល់គ្នា (MoU) រយៈពេល ៦០ថ្ងៃ ដែលមានគោលបំណងពន្យារក្របខណ្ឌបទឈប់បាញ់ដែលមានស្រាប់។ ទោះជាយ៉ាងណា មិនមានកិច្ចព្រមព្រៀងផ្លូវការណាមួយត្រូវបានចុះហត្ថលេខានោះទេ។

ក្នុងពេលជាមួយគ្នានេះ ភាពតានតឹងរវាងអ៊ីស្រាអែល និងលីបង់នៅតែមានកម្រិតខ្ពស់ ដោយការបាញ់ប្រហារគ្នានៅតាមព្រំដែននៅតែបន្ត។ ក្រុម Hezbollah ដែលទទួលបានការគាំទ្រពីអ៊ីរ៉ង់ នៅតែជាភាគីសំខាន់មួយក្នុងជម្លោះនេះ ខណៈសហរដ្ឋអាមេរិកបន្តគាំទ្រអ៊ីស្រាអែល។ ជាលទ្ធផល ការចរចាណាមួយនាពេលអនាគតដែលពាក់ព័ន្ធនឹងអ៊ីរ៉ង់ ទំនងជានឹងត្រូវបានជះឥទ្ធិពលដោយការពិចារណាផ្នែកសន្តិសុខក្នុងតំបន់ ដោយអ៊ីរ៉ង់ទាមទារឱ្យមានបទឈប់បាញ់រវាងអ៊ីស្រាអែល និងលីបង់ជាលក្ខខណ្ឌជាមុនសម្រាប់កិច្ចព្រមព្រៀងបទឈប់បាញ់ណាមួយជាមួយសហរដ្ឋអាមេរិក។

ភាពមិនច្បាស់លាស់ដែលបន្តមាននៅមជ្ឈិមបូព៌ាបានជួយរក្សាតម្លៃប្រេងឱ្យស្ថិតក្នុងកម្រិតខ្ពស់ពេញមួយខែឧសភា ដែលបង្កើនក្តីបារម្ភអំពីអតិផរណា និងធ្វើឱ្យទីផ្សារមានភាពប្រតិកម្មកាន់តែខ្លាំងចំពោះការវិវត្តន៍ភូមិសាស្ត្រនយោបាយ។ សម្រាប់វិនិយោគិន ឥទ្ធិពលលើតម្លៃមាសនៅតែអាស្រ័យលើតុល្យភាពរវាងការរំពឹងទុកអតិផរណា ការរំពឹងទុកអត្រាការប្រាក់ និងតម្រូវការទ្រព្យសុវត្ថិភាព (Safe-Haven Asset) ។

ចំណុចសំខាន់សម្រាប់មាស៖

- ប្រសិនបើភាពតានតឹងនៅតែបន្ត ឬកើនឡើង តម្លៃប្រេងខ្ពស់អាចបង្កើនសម្ពាធអតិផរណា ដែលអាចជំរុញឱ្យធនាគារកណ្តាលអាមេរិករក្សាអត្រាការប្រាក់ក្នុងកម្រិតខ្ពស់រយៈពេលយូរ ដែលអាចធ្វើឲមានសម្ពាធអវិជ្ចមានទៅលើតម្លៃមាស។ ទោះជាយ៉ាងណា ភាពមិនច្បាស់លាស់ផ្នែកភូមិសាស្ត្រនយោបាយក៏អាចបង្កើនតម្រូវការមាសជាទ្រព្យសុវត្ថិភាព (Safe-Haven Asset) ផងដែរ។

- ប្រសិនបើភាពតានតឹងថយចុះ និងតម្លៃថាមពលធ្លាក់ចុះ ក្តីបារម្ភអំពីអតិផរណាអាចថយចុះជាបណ្តើរៗ ដែលបង្កើនលទ្ធភាពនៃការបន្ធូរបន្ថយគោលនយោបាយរូបិយវត្ថុនាពេលអនាគត។ ការរំពឹងទុកអត្រាការប្រាក់ទាបជាទូទៅគាំទ្រដល់តម្លៃមាស ប៉ុន្តែការថយចុះនៃតម្រូវការទ្រព្យសុវត្ថិភាព (Safe-Haven Asset) អាចកាត់បន្ថយឥទ្ធិពលវិជ្ជមាននេះបានខ្លះ។

ជារួម ការវិវត្តន៍ភូមិសាស្ត្រនយោបាយនៅតែជាកត្តាសំខាន់ដែលមានឥទ្ធិពលទាំងលើការរំពឹងទុកអតិផរណា និងតម្រូវការរបស់វិនិយោគិនចំពោះទ្រព្យសុវត្ថិភាព (Safe-Haven Asset) ដូចជាមាស។

ការវិភាគបច្ចេកទេស

ទិដ្ឋភាពទូទៅនៃទីផ្សារមាស — ខែមិថុនា ឆ្នាំ 2026

បច្ចុប្បន្ន មាសកំពុងជួញដូរនៅតម្លៃ 4,328.00 ដុល្លារ ដោយបន្តសន្ទុះធ្លាក់ចុះយ៉ាងខ្លាំងក្លា ។ គំនូសតាងបង្ហាញពីសម្ពាធនៃការលក់យ៉ាងខ្លាំង ខណៈដែលតម្លៃត្រូវបានរុញច្រានចូលទៅក្នុងតំបន់ low-volume ដែលបានបង្កើតឡើងក្នុងរយៈពេលប៉ុន្មានខែថ្មីៗនេះ ។

តំបន់បច្ចេកទេសសំខាន់ៗ

- តម្លៃបច្ចុប្បន្ន៖ 4,328.00 ដុល្លារ — កំពុងជួញដូរចំតំបន់ low-volume ក្នុងប្រវត្តិសាស្ត្រពីប៉ុន្មានខែមុន ។ ជាទូទៅ តំបន់ low-volume ផ្តល់នូវកម្រិតទប់ (support) ខ្សោយ ដែលបង្ហាញពីចំណុចដ៏សំខាន់មួយសម្រាប់ការធ្លាក់ចុះយ៉ាងឆាប់រហ័សដែលអាចកើតមាន ។

- Major Supply Zone នៅតម្លៃ 4,426.00 ដុល្លារ៖ គឺជាតំបន់រារាំង (resistance) ខាងលើភ្លាមៗ ដែលអ្នកលក់ទំនងជានឹងឈានជើងចូលទីផ្សារវិញក្នុងអំឡុងពេលមានការងើបឡើងវិញរយៈពេលខ្លីណាមួយ ។

- Last Month Point of Control (POC) នៅតម្លៃ 4,544.00 ដុល្លារ៖ ជាកម្រិតទំហំជួញដូរខ្ពស់បំផុតពីខែមុន ដែលដើរតួជាកម្រិតរារាំងរចនាសម្ព័ន្ធដ៏សំខាន់ និងបង្ហាញពីកន្លែងដែលអ្នកចូលរួមក្នុងទីផ្សារធ្លាប់ទទួលបានតម្លៃខ្ពស់បំផុត ។

យុទ្ធសាស្ត្រជួញដូរ

- Bearish Bias: និន្នាការបច្ចុប្បន្ននៅតែបន្តធ្លាក់ចុះយ៉ាងខ្លាំង ។ ការចូលទៅក្នុងតំបន់ low-volume បង្ហាញពីកង្វះចំណាប់អារម្មណ៍របស់អ្នកទិញក្នុងប្រវត្តិសាស្ត្រ ដែលបង្កើនលទ្ធភាពនៃការបន្តធ្លាក់ចុះបន្ថែមទៀត ។ ពាណិជ្ជករដែលស្វែងរកឱកាសទិញ (long) គួរតែមានការប្រុងប្រយ័ត្នខ្ពស់ ដោយសារប្រូបាប៊ីលីតេនៃការវិលត្រឡប់មកវិញប្រកបដោយនិរន្តរភាពមានកម្រិតទាបនៅដំណាក់កាលនេះ ។

- Continuation/Pullback Scenario: ប្រសិនបើតម្លៃអាចបំបែក និងបន្តជួញដូរនៅក្រោមតម្លៃបច្ចុប្បន្ន 4,328.00 ដុល្លារ នោះសន្ទុះនៃការធ្លាក់ចុះត្រូវបានរំពឹងថានឹងកើនឡើងយ៉ាងឆាប់រហ័ស ដោយសារកង្វះការគាំទ្រពីទំហំជួញដូរនៅខាងក្រោម ។ ផ្ទុយទៅវិញ ប្រសិនបើមានការងើបឡើងវិញរយៈពេលខ្លីកើតចេញពីកម្រិតនេះ ទីផ្សារអាចនឹងសាកល្បង Major Supply Zone នៅតម្លៃ 4,426.00 ដុល្លារម្តងទៀត ដែលអាចផ្តល់នូវឱកាសថ្មីសម្រាប់ការចូលលក់ (short entries) ។

| English Version |

This report provides an analysis of the primary factors influencing gold prices, offering insights for investors.

Disclaimer: All information presented is for educational purposes only and should not be interpreted as financial advice or a recommendation for trading or investment decisions.

Fundamental Analysis

Previous Recap of the Whole Economy: In May 2026, global financial markets operated in a mixed macroeconomic environment, where growth remained broadly resilient but lacked clear momentum. While recession fears did not intensify, uncertainty persisted as investors continued to reassess the timing and direction of monetary policy shifts amid uneven inflation progress across major economies.

In the United States, economic activity remained stable, supported by steady consumer demand and a still-healthy labor market. However, inflation continued to show signs of persistence in certain components, particularly services, keeping the Federal Reserve cautious. As a result, expectations for near-term rate cuts were repeatedly pushed back, contributing to a more data-dependent and reactive market environment.

US Treasury yields remained elevated and volatile throughout the month, reflecting ongoing concerns around sticky inflation, fiscal outlook uncertainty, and shifting rate expectations rather than a strong reacceleration in growth. This dynamic kept financial conditions relatively tight and limited the scope for broad risk appetite expansion.

Outside the US, Europe continued to show subdued growth momentum, with weak industrial activity weighing on overall sentiment despite some signs of stabilization in services. China maintained a gradual recovery path, supported by targeted policy support measures, although the pace of improvement remained uneven and below earlier expectations.

Overall, global macro conditions remained in a “wait-and-see” phase, with markets highly sensitive to inflation data, central bank communication, and geopolitical developments. Within this environment, gold prices remained supported as investors continued to hedge against policy uncertainty, inflation persistence, and broader macro risks. Despite elevated real yields at times, gold held its ground, reflecting its continued role as a defensive asset in an uncertain macro backdrop.

Upcoming Federal Interest Rate Decision

What factors should be considered before the upcoming U.S. interest rate decision next week?

Labor Market: The U.S. labor market remains relatively resilient, as reflected in the latest employment data. Nonfarm Payrolls (NFP) continued to show job growth above market expectations, while the unemployment rate remained stable. At the same time, Average Hourly Earnings continued to indicate steady wage growth, suggesting that underlying labor market conditions remain healthy despite signs of gradual moderation compared to previous years.

A resilient labor market provides the Federal Reserve with greater flexibility to maintain its current policy stance, as policymakers remain focused on ensuring inflation returns sustainably to its target.

Inflation: With labor market conditions remaining stable, inflation is likely to be the most important factor influencing the Federal Reserve’s interest rate decision. Upcoming CPI and PPI releases will provide further insight into current price pressures and whether inflation continues to moderate toward the Fed’s 2% target.

The most likely scenario is that inflation remains moderately elevated but broadly in line with market expectations. If this occurs, the Federal Reserve is expected to keep interest rates unchanged while maintaining a cautious, data-dependent approach at the next Federal Open Market Committee (FOMC) meeting. Such an outcome would reinforce expectations that interest rates may remain higher for longer rather than signal an immediate shift toward monetary easing.

The upcoming meeting will also be the first FOMC meeting chaired by Kevin Warsh following his appointment as Federal Reserve Chair in May 2026. While monetary policy decisions remain data-dependent, investors will closely monitor the policy statement, economic projections, and press conference for any indications of how the new leadership may approach inflation, interest rates, and future policy guidance.

According to current market pricing reflected in the CME FedWatch Too below, investors generally expect the Federal Reserve to maintain its current policy rate in the near term, with future policy decisions remaining highly dependent on incoming inflation and labor market data.

For gold, a prolonged higher-interest-rate environment could limit upside momentum by supporting U.S. Treasury yields and the U.S. dollar. However, ongoing geopolitical risks, fiscal uncertainty, and safe-haven demand may continue to provide underlying support, suggesting that gold’s outlook will remain closely tied to both inflation developments and broader market sentiment.

Geopolitical Tension

U.S.-China Trade War: U.S. President Donald Trump met with Chinese President Xi Jinping during the U.S.-China Summit from May 13 to May 15. The discussions focused primarily on trade, investment, and broader economic cooperation between the world’s two largest economies. While no major breakthrough was announced, both sides agreed to expand dialogue through new trade and investment cooperation mechanisms and signaled a willingness to reduce certain trade barriers. Progress was also reported in areas such as agricultural trade, aircraft purchases, and discussions surrounding reciprocal tariff reductions. Overall, the summit helped improve market sentiment by reducing concerns over a further escalation of U.S.-China trade tensions. Investors will continue monitoring developments closely, with President Xi expected to visit the White House later this year for a follow-up summit.

U.S.-Iran Conflict and Middle East Developments: May saw continued developments surrounding the conflict involving the United States and Iran. Reports emerged that both sides were discussing a potential 60-day memorandum of understanding (MoU) aimed at extending the existing ceasefire framework. However, no formal agreement was ultimately signed.

At the same time, tensions between Israel and Lebanon remained elevated, with exchanges of fire continuing across the border. Iran-backed Hezbollah remains a key participant in the conflict, while the United States continues to support Israel. As a result, any future negotiations involving Iran are likely to be influenced by broader regional security considerations with Iran demanding that a ceasefire between Israel and Lebanon to be a precondition for any ceasefire agreement with the U.S.

The ongoing uncertainty in the Middle East helped keep oil prices elevated throughout May, contributing to inflation concerns and increasing market sensitivity to geopolitical developments. For investors, the impact on gold remains dependent on the balance between inflation expectations, interest rate expectations, and safe-haven demand.

Key Takeaway for Gold

- If tensions persist or escalate, higher oil prices could contribute to stronger inflation pressures, potentially encouraging the Federal Reserve to maintain a higher-for-longer interest rate stance, which could pressure gold prices. However, heightened geopolitical uncertainty could also increase safe-haven demand for gold.

- If tensions ease and energy prices moderate, inflation concerns may gradually decline, increasing the likelihood of future monetary policy easing. Lower interest rate expectations would generally be supportive for gold, although reduced safe-haven demand could partially offset this effect.

Overall, geopolitical developments remain an important factor influencing both inflation expectations and investor demand for safe-haven assets such as gold.

Technical Analysis

Gold Market Overview — 9th June 2026

Gold is currently trading at $4,328.00, continuing its aggressive bearish momentum. The chart reveals strong selling pressure as the price pushes into the low-volume areas established over the last few months.

Key Technical Zones

- Current Price: $4,328.00 — Trading exactly at a historical low-volume zone from the previous months. Low-volume areas typically offer weak support, indicating a critical juncture for potential rapid downside movement.

- Major Supply Zone at $4,426.00: The immediate overhead resistance area where sellers are likely to step back into the market during any short-term relief rallies.

- Last Month Point of Control (POC) at $4,544.00: The highest volume level from last month, acting as a major structural resistance and indicating where market participants previously found the most value.

Trading Strategy

- Bearish Bias: The current trend remains strongly bearish. Entering a low-volume zone suggests a lack of historical buyer interest, which increases the likelihood of further downside continuation. Traders looking for long opportunities should remain highly cautious, as the probability of a sustained reversal is low at this stage.

- Continuation/Pullback Scenario: If the price cleanly breaks and sustains trading below the current $4,328.00 level, the bearish momentum is expected to accelerate rapidly due to the lack of volume support below. Conversely, if a short-term bounce occurs from this level, the market could retest the major supply area at $4,426.00, which may provide new opportunities for short entries.