កិច្ចប្រជុំកំពូល និងសង្គ្រាមពាណិជ្ជកម្មរវាងសហរដ្ឋអាមេរិក និងចិន

ប្រធានាធិបតីសហរដ្ឋអាមេរិក លោក Donald Trump គ្រោងជួបជាមួយប្រធានាធិបតីចិន លោក Xi Jinping នៅទីក្រុងប៉េកាំង សម្រាប់កិច្ចប្រជុំកំពូលរវាងសហរដ្ឋអាមេរិក និងចិន ដែលប្រព្រឹត្តទៅចាប់ពីថ្ងៃទី១៣ ដល់ថ្ងៃទី១៥ ខែឧសភា។

ទីផ្សារកំពុងតាមដានកិច្ចប្រជុំនេះយ៉ាងដិតដល់ ដើម្បីស្វែងរកសញ្ញាពាក់ព័ន្ធនឹងពន្ធគយ ទំនាក់ទំនងពាណិជ្ជកម្មរវាងសហរដ្ឋអាមេរិក និងចិន សង្គ្រាមអ៊ីរ៉ង់ និងបញ្ហាភូមិសាស្ត្រនយោបាយផ្សេងៗទៀត។ យោងតាមស្ថាប័ន Brookings Institution លទ្ធផលដែលមានភាគរយកើតឡើងខ្ពស់បំផុត គឺការបន្តបទឈប់បាញ់ពាណិជ្ជកម្មបច្ចុប្បន្ន មិនមែនការដោះស្រាយភាពតានតឹងទាំងស្រុងទេ។ ការបន្តបទឈប់បាញ់ពាណិជ្ជកម្មនេះអាចជួយកាត់បន្ថយភាពប្រែប្រួលក្នុងទីផ្សារហិរញ្ញវត្ថុសកលក្នុងរយៈពេលខ្លី។

ទោះបីជាភាពតានតឹងរវាងមហាអំណាចសេដ្ឋកិច្ចទាំងពីរកំពុងមានសញ្ញាធូរស្រាលក៏ដោយ ការប្រកួតប្រជែងយុទ្ធសាស្ត្រ និងសង្គ្រាមពាណិជ្ជកម្មរវាងសហរដ្ឋអាមេរិក និងចិន ត្រូវបានគេរំពឹងថានឹងបន្តទៀតនៅអនាគត។ ស្របពេលដែលភាពតានតឹងភូមិសាស្ត្រនយោបាយកើនឡើង ការចំណាយយោធារបស់សហរដ្ឋអាមេរិកក៏នៅតែមានកម្រិតខ្ពស់ផងដែរ ដោយសំណើថវិកាការពារជាតិសម្រាប់ឆ្នាំសារពើពន្ធ FY2027 ត្រូវបានរាយការណ៍ថាអាចឈានដល់ 1.5 ទ្រីលានដុល្លារអាមេរិក ដែលជាសំណើថវិកាធំបំផុតក្នុងប្រវត្តិសាស្ត្រសហរដ្ឋអាមេរិក។ ទន្ទឹមនឹងនេះ ប្រទេសចិនក៏បន្តគោលដៅរយៈពេលវែងរបស់ខ្លួនក្នុងការពង្រឹងខ្លួនបន្តទៀតជាមហាអំណាចសេដ្ឋកិច្ច និងបច្ចេកវិទ្យាសកល។

ដើម្បីសម្រេចគោលដៅនោះ ចិនបានទទួលស្គាល់ពីភាពចាំបាច់ក្នុងការកាត់បន្ថយការពឹងផ្អែកសកលលើប្រាក់ដុល្លារអាមេរិកដូចដែលបានឆ្លុះបញ្ចាំងតាមរយៈការពិភាក្សារបស់ក្រុមប្រទេស BRICS ក្នុងការស្វែងរកជម្រើសផ្សេងៗដើម្បីកាត់បន្ថយឥទ្ធិពលរបស់ប្រាក់ដុល្លារ។ ទោះជាយ៉ាងណា លោក Donald Trump បានឆ្លើយតបយ៉ាងម៉ឺងម៉ាត់ ដោយមានប្រសាសន៍ថា៖ “យើងទាមទារឱ្យប្រទេសទាំងនេះប្តេជ្ញាថា ពួកគេនឹងមិនបង្កើតរូបិយប័ណ្ណ BRICS ថ្មី ឬគាំទ្ររូបិយប័ណ្ណផ្សេងណាមួយដើម្បីជំនួសប្រាក់ដុល្លារអាមេរិកដ៏មានអំណាចនោះឡើយ។ បើមិនដូច្នេះទេ ពួកគេនឹងប្រឈមនឹងពន្ធគយ 100% និងការរារាំងមិនឪ្យចូលមកទីផ្សារសេដ្ឋកិច្ចដ៏អស្ចារ្យរបស់សហរដ្ឋអាមេរិក។”

យ៉ាងណាក៏ដោយ ប្រាក់ដុល្លារអាមេរិកនៅតែជារូបិយប័ណ្ណសកលសំខាន់ ដោយមានចំណែកប្រហែល 56.77% នៃទុនបម្រុងរូបិយប័ណ្ណបរទេសសកលក្នុងត្រីមាសទី៤ ឆ្នាំ២០២៥ ខណៈប្រាក់យ័នចិន មានចំណែកប្រហែល 1.95% ប៉ុណ្ណោះ យោងតាមទិន្នន័យរបស់ IMF។

អាស្រ័យលើលទ្ធផលនៃកិច្ចប្រជុំកំពូលនេះ អារម្មណ៍ទីផ្សារអាចប្រែប្រួលយ៉ាងខ្លាំង។

- លទ្ធផលវិជ្ជមានដែលអាចកាត់បន្ថយភាពតានតឹងពាណិជ្ជកម្ម អាចជួយគាំទ្រចំណង់ហានិភ័យ (Risk Appetite) និងទីផ្សារភាគហ៊ុនសកល ខណៈដែលអាចដាក់សម្ពាធលើទ្រព្យសកម្មសុវត្ថិភាព (Safe-Haven Assets) ដូចជាមាសជាដើម។

- ផ្ទុយទៅវិញ ប្រសិនបើភាពតានតឹងកើតឡើងវិញ ឬមានវិធានការពាណិជ្ជកម្មតឹងរ៉ឹងជាងមុន នោះវាអាចបង្កើនតម្រូវការលើទ្រព្យសកម្មសុវត្ថិភាព រួមមានទាំងប្រាក់ដុល្លារអាមេរិក និងមាស។

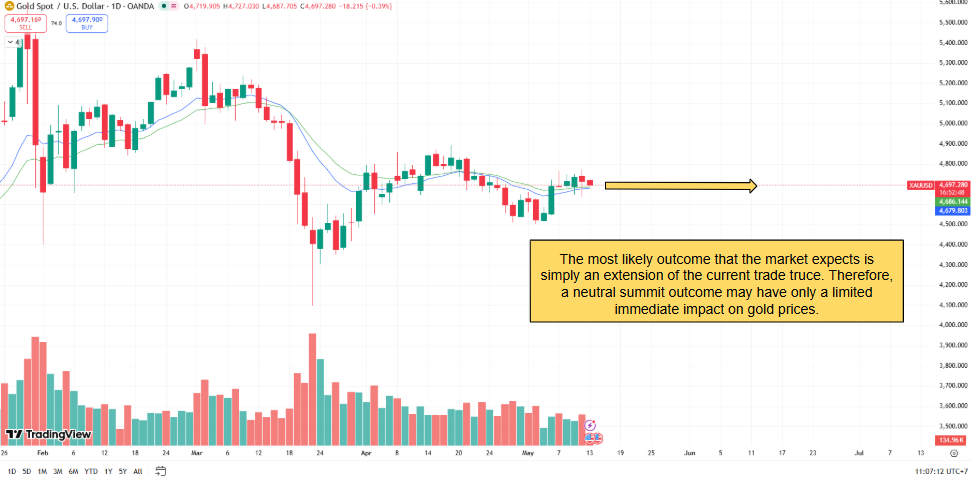

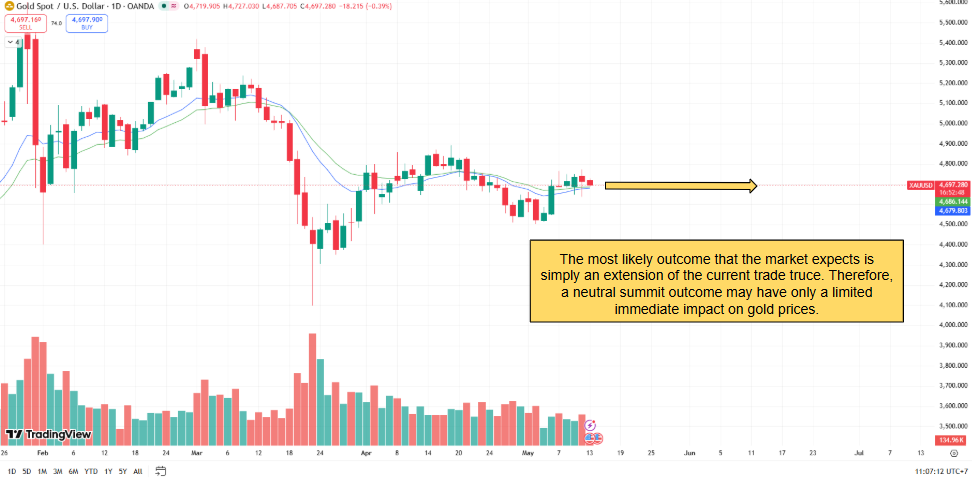

- ទោះជាយ៉ាងណា ដោយសារទីផ្សារភាគច្រើនបានរំពឹងទុករួចហើយថា បទឈប់បាញ់ពាណិជ្ជកម្មបច្ចុប្បន្ននឹងត្រូវបានបន្ត ដូច្នេះលទ្ធផលអព្យាក្រឹតពីកិច្ចប្រជុំអាចមានផលប៉ះពាល់តិចតួចប៉ុណ្ណោះទៅលើតម្លៃមាស លុះត្រាតែមានការប្រកាសគោលនយោបាយ ឬការ

វិវត្តភូមិសាស្ត្រនយោបាយដែលមិនបានរំពឹងទុក។

វិនិយោគិនគួរបន្តតាមដានការវិវត្តន៍ពីកិច្ចប្រជុំនេះយ៉ាងដិតដល់ ព្រោះការប្រកាសសំខាន់ៗណាមួយអាចជះឥទ្ធិពលយ៉ាងខ្លាំងដល់ទីផ្សារហិរញ្ញវត្ថុសកល។

ការចេញផ្សាយទិន្នន័យសេដ្ឋកិច្ចសហរដ្ឋអាមេរិក – សន្ទស្សន៍តម្លៃទំនិញប្រើប្រាស់ (CPI) និងសន្ទស្សន៍តម្លៃអ្នកផលិត (PPI)

នៅថ្ងៃទី១២ ខែឧសភា ទិន្នន័យសន្ទស្សន៍តម្លៃទំនិញប្រើប្រាស់ (CPI) ចុងក្រោយរបស់សហរដ្ឋអាមេរិកបានបង្ហាញថា សម្ពាធអតិផរណានៅតែមានកម្រិតខ្ពស់ក្នុងខែមេសា។ សន្ទស្សន៍តម្លៃទំនិញប្រើប្រាស់ (CPI) ប្រចាំឆ្នាំ (YoY) បានកើនឡើងដល់ 3.8% ពី 3.3% ខណៈ សន្ទស្សន៍តម្លៃទំនិញប្រើប្រាស់មូលដ្ឋាន (Core CPI) ប្រចាំខែ (MoM) បានកើនឡើងដល់ 0.4% ពី 0.2% ដែលបង្ហាញថាសម្ពាធអតិផរណាមូលដ្ឋាននៅតែបន្តមានការកើនឡើង។ ទន្ទឹមនឹងនេះ សន្ទស្សន៍តម្លៃទំនិញប្រើប្រាស់ (CPI) ប្រចាំខែ (MoM) បានថយចុះមកនៅ 0.6% ពី 0.9% ដែលបង្ហាញថា ទោះបីអតិផរណានៅតែខ្ពស់ក៏ដោយ កំណើនតម្លៃទំនិញអាចកំពុងចាប់ផ្តើមថយល្បឿនបន្តិច។

សម្រាប់ទីផ្សារមាស អតិផរណាដែលនៅតែខ្ពស់អាចពង្រឹងការរំពឹងទុកថា ធនាគារកណ្តាលសហរដ្ឋអាមេរិក (Federal Reserve) អាចរក្សាអត្រាការប្រាក់នៅកម្រិតខ្ពស់រយៈពេលយូរជាងមុន ដែលអាចជួយគាំទ្រប្រាក់ដុល្លារអាមេរិក ហើយដាក់សម្ពាធលើតម្លៃមាស។

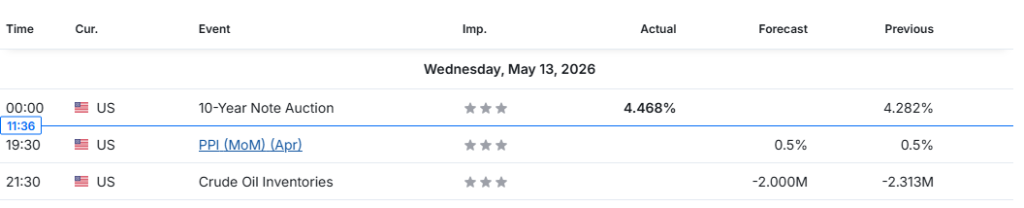

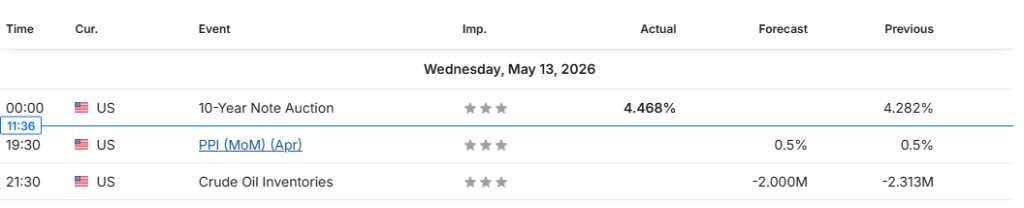

អ្នកជួញដូរគួរតែបន្តតាមដាន សន្ទស្សន៍តម្លៃអ្នកផលិត (PPI) របស់សហរដ្ឋអាមេរិក ដែលនឹងចេញផ្សាយនៅល្ងាចនេះ ថ្ងៃទី 13 ខែឧសភា វេលាម៉ោង 7:30 យប់ (GMT+7)។

| English Version |

U.S.-China Summit and Trade War

U.S. President Donald Trump is set to meet with Chinese President Xi Jinping in Beijing for the U.S.-China summit from May 13th to May 15th.

Markets are closely monitoring the summit for signals regarding tariffs, trade relations between the U.S. and China, the Iran War, and other geopolitical developments. According to the Brookings Institution, the most likely outcome is an extension of the current trade truce rather than a complete resolution of tensions, which could help limit near-term volatility across global markets.

Despite the current easing of tensions between the two global powerhouses, strategic competition and the ongoing trade war between the United States and China are expected to remain long-term themes. Amid rising geopolitical tensions, U.S. defense spending also remains elevated, with the FY2027 U.S. defense budget proposal reportedly reaching USD 1.5 trillion, the largest proposal in U.S. history. Meanwhile, China continues pursuing its long-term objective of strengthening its position as a global economic and technological powerhouse.

To achieve that goal, China recognizes the need to reduce global reliance on the U.S. Dollar, as reflected in ongoing BRICS discussions exploring alternatives to dollar dominance. However, President Donald Trump responded firmly, stating, “We require a commitment from these seemingly hostile countries that they will neither create a new BRICS currency nor back any other currency to replace the mighty U.S. dollar. Otherwise, they will face 100% tariffs and should expect to say goodbye to selling into the wonderful U.S. economy.”

Regardless, the U.S. Dollar remains the de facto global currency, accounting for approximately 56.77% of global foreign-exchange reserves in Q4 2025, while the Chinese Yuan accounted for approximately 1.95%, according to IMF data.

Depending on the outcome of the summit, market sentiment could shift significantly.

- A constructive outcome that reduces trade tensions may support risk appetite and global equities while placing downward pressure on safe-haven assets such as gold.

- Conversely, renewed tensions or tougher trade measures could increase demand for traditional safe havens, including both the U.S. Dollar and gold.

- However, since markets already largely expect an extension of the current trade truce, a neutral summit outcome may have only a limited immediate impact on gold prices unless accompanied by unexpected policy announcements or geopolitical developments.

Traders should continue monitoring developments from the summit closely, as any major announcements could significantly impact global financial markets.

Economic Data Release – CPI and Upcoming PPI Release

On May 12th, the latest U.S. CPI data indicated that inflationary pressures remained elevated in April. CPI year-over-year rose to 3.8% from the previous 3.3%, while Core CPI month-over-month accelerated to 0.4% from 0.2% previously, signaling persistent underlying inflation. Meanwhile, monthly CPI slowed to 0.6% from the previous 0.9%, suggesting that although inflation remains high, the pace of price increases may be moderating slightly. For the gold market, persistent inflation could reinforce expectations that the Federal Reserve may keep interest rates elevated for longer, potentially supporting the U.S. Dollar and placing downward pressure on gold prices. Traders should now look ahead to the PPI that will be released later today, on May 13th at 7:30 PM GMT+7.