របាយការណ៍សង្ខេបទិន្នន័យប្រចាំសប្តាហ៍

គិតត្រឹមថ្ងែទី 19 ខែឧសភា ឆ្នាំ2026

ខាងក្រោមនេះគឺជារបាយការណ៍សង្ខេបស្ថានភាពនៅសហរដ្ឋអាមេរិក ដែលផ្តោតលើព្រឹត្តិការណ៍សំខាន់ៗពាក់ព័ន្ធនឹងប្រធានាធិបតី លោក Donald Trump ទិន្នន័យសេដ្ឋកិច្ច និងភាពតានតឹងភូមិសាស្ត្រនយោបាយក្នុងសប្តាហ៍កន្លងមក។

ការបដិសេធ (Disclaimer): របាយការណ៍នេះធ្វើឡើងក្នុងគោលបំណងផ្សព្វផ្សាយការអប់រំ និងព័ត៌មានដែលគួរដឹងតែប៉ុណ្ណោះ។ សូមមេត្តាកំុប្រើប្រាស់វាជាដំបូន្មានវិនិយោគ ឬជាសញ្ញាសម្រាប់ការជួញដូររបស់អ្នក។

ព័ត៌មានសំខាន់ៗនៅក្នុងសប្តាហ៍នេះ

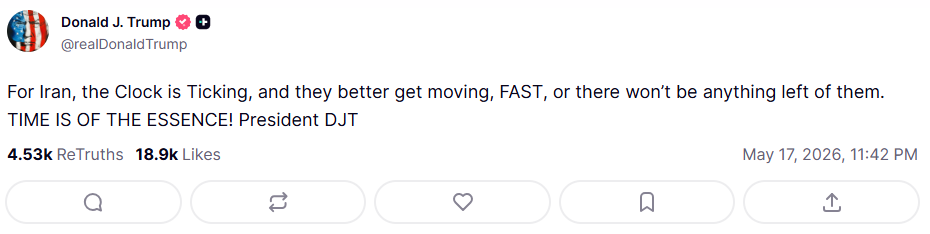

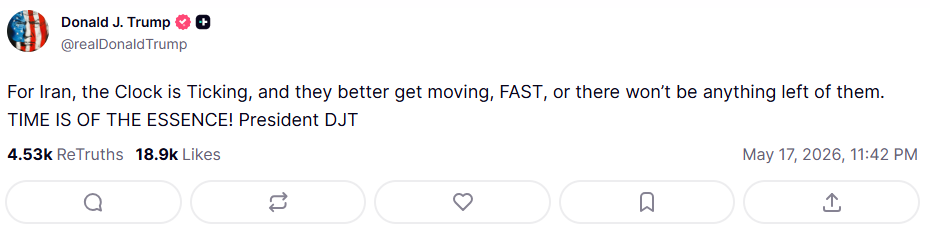

ជម្លោះសហរដ្ឋអាមេរិក និងអ៊ីរ៉ង់៖ ក្នុងសប្តាហ៍កន្លងមក ការរំពឹងទុកអំពីកិច្ចព្រមព្រៀងសន្តិភាពរវាងសហរដ្ឋអាមេរិក និងអ៊ីរ៉ង់បានថយចុះ។ សហរដ្ឋអាមេរិកបានដាក់សំណើមួយទៅអ៊ីរ៉ង់ ខណៈអ៊ីរ៉ង់បានឆ្លើយតបវិញដោយសំណើប្រឆាំង ដែលបន្ទាប់មកត្រូវបានប្រធានាធិបតី លោក Donald Trump ពិពណ៌នាថា “មិនអាចទទួលយកបាន”។ បន្ថែមពីនេះ នៅថ្ងៃទី 18 ខែឧសភា ឆ្នាំ 2026 លោក Donald Trump បានបង្ហោះសារនៅលើ Truth Social ថា៖

“ពេលវេលាជិតអស់ហើយសម្រាប់អ៊ីរ៉ង់។ ពួកគេត្រូវតែចាត់វិធានការឱ្យបានលឿន។”

សរុបមក ភាពតានតឹងរវាងប្រទេសទាំងពីរមានការកើនឡើង ហើយក៏អាចកើនឡើងបន្ថែមនៅពេលខាងមុខដែរ។ ដោយសារភាពមិនប្រាកដប្រជានៃស្ថានភាពភូមិសាស្ត្រនយោបាយ តម្លៃកិច្ចសន្យាគម្លាតថ្លៃប្រេង Brent (Brent Oil CFDs) និងតម្លៃកិច្ចសន្យាគម្លាតថ្លៃប្រេងឆៅ WTI (WTI Crude Oil CFDs) បានកើនឡើងបន្តិចក្នុងសប្តាហ៍មុននេះ។

កិច្ចប្រជុំកំពូលសហរដ្ឋអាមេរិក និងចិន៖ ប្រធានាធិបតី លោក Donald Trump បានជួបប្រជុំជាមួយប្រធានាធិបតី លោក Xi Jinping ក្នុងសប្តាហ៍មុន សម្រាប់កិច្ចប្រជុំកំពូលរវាងសហរដ្ឋអាមេរិក និងចិន។ កិច្ចប្រជុំនេះក៏មានការចូលរួមពី នាយកប្រតិបត្តិកំពូលនៃប្រទេសទាំងពីរផងដែរ ដូចជា Elon Musk (Tesla), Jensen Huang (Nvidia) និង Lei Jun (Xiaomi)។ ទោះបីភាគីទាំងពីរបានអះអាងថាកិច្ចពិភាក្សាមានប្រសិទ្ធភាព ក៏ដោយ ប៉ុន្តែជាក់ស្តែងគឺមិនមានកិច្ចព្រមព្រៀងធំៗលើប្រធានបទសំខាន់ៗ ដូចជា ពន្ធនាំចូល ឬការពន្យារពេលសន្ធិសញ្ញាពាណិជ្ជកម្មឡើយ។

យ៉ាងណាក៏ដោយ ទំនាក់ទំនងរវាងប្រទេសទាំងពីរបានប្រសើរឡើងបន្តិច ហើយភាពតានតឹងបានធ្លាក់ចុះ។ លោក Xi Jinping ក៏ត្រូវបានរំពឹងថានឹងទៅទស្សនកិច្ចសេតវិមាននៅរដូវស្លឹកឈើជ្រុះសម្រាប់កិច្ចប្រជុំបន្ត។ តម្លៃមាសបានធ្លាក់ចុះបន្តិចក្នុងសប្តាហ៍មុន ប្រហែលដោយសារការកាត់បន្ថយតម្រូវការរទ្រព្យសកម្មសុវត្ថិភាព (Safe-Haven Assets)។

ការតែងតាំង លោក Kevin Warsh ជាប្រធានធនាគារកណ្តាលថ្មី:

សប្តាហ៍មុន គឺជាការបញ្ជាក់ជាផ្លូវការនៃការតែងតាំង លោក Kevin Warsh ជាប្រធានថ្មីនៃធនាគារកណ្តាលអាមេរិក។

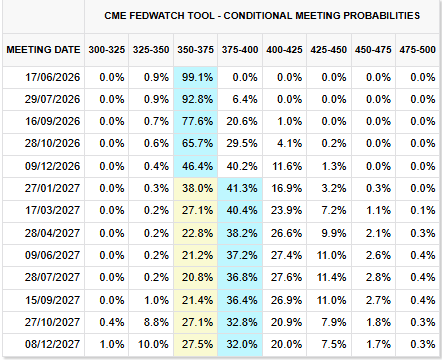

បច្ចុប្បន្ន ធនាគារកណ្តាលអាមេរិកនៅតែរក្សាអត្រាការប្រាក់ក្នុងកម្រិតខ្ពស់ ហើយក៏មានលទ្ធភាពក្នុងការកើនឡើងបន្ថែមដែរ។ ប៉ុន្តែ ការតែងតាំង លោក Kevin Warsh ក៏អាចផ្លាស់ប្តូរទិសដៅគោលនយោបាយរបស់ធនាគារកណ្តាលអាមេរិកដែរ។

បើអត្រាការប្រាក់កើនឡើង តម្លៃមាសអាចធ្លាក់ចុះ ដោយសារតម្លៃប្រាក់ដុល្លារអាមេរិកកាន់តែរឹងមាំ។ ផ្ទុយទៅវិញ បើអត្រាការប្រាក់ត្រូវបានកាត់បន្ថយ តម្លៃមាសអាចកើនឡើង។ ទោះជាយ៉ាងណា ក្នុងរយៈពេលខ្លីខាងមុខ អត្រាការប្រាក់ប្រហែលនឹងនៅតែដដែលទេ។

ទិន្នន័យសេដ្ឋកិច្ចសំខាន់ៗរបស់សហរដ្ឋអាមេរិក៖

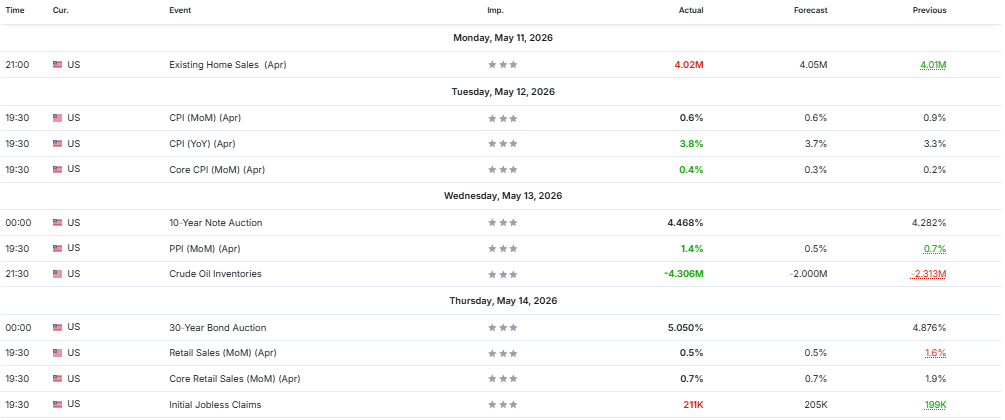

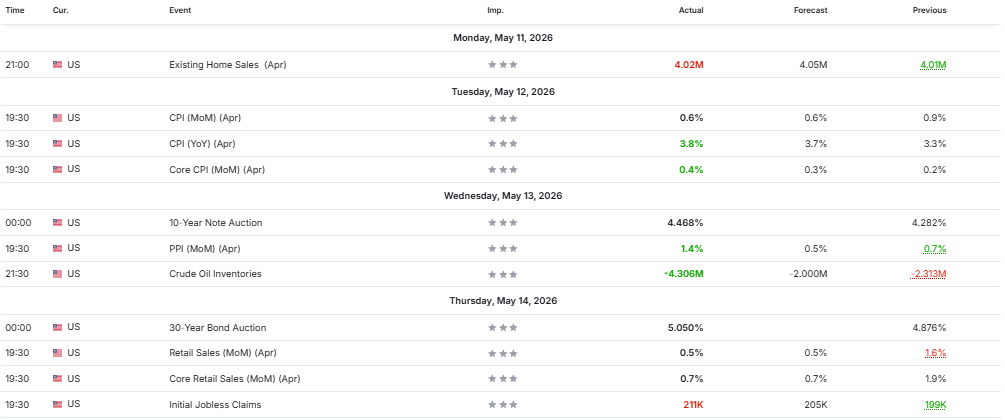

ទិន្នន័យចុងក្រោយបង្ហាញពីភាពចម្រុះនៅក្នុងសេដ្ឋកិច្ចសហរដ្ឋអាមេរិក ប៉ុន្តែមាននិន្នាការកើនឡើងនៃអតិផរណាបន្តិច។ សន្ទស្សន៍តម្លៃទំនិញប្រើប្រាស់ប្រចាំខែ (CPI MoM) នៅតែថេរ តែសន្ទស្សន៍តម្លៃទំនិញប្រើប្រាស់ប្រចាំឆ្នៃ (CPI YoY) កើនដល់ 3.8% ខណៈតម្លៃទំនិញប្រើប្រាស់មូលដ្ឋាន (Core CPI) ក៏លើសការរំពឹងទុក បង្ហាញពីសម្ពាធតម្លៃនៅតែមាន។ សន្ទស្សន៍តម្លៃអ្នកផលិត (PPI) ក៏កើនលើសការរំពឹងទុក បញ្ជាក់ពីអតិផរណាដែលនៅតែបន្ត។

រីឯផ្នែកកំណើនសេដ្ឋកិច្ចវិញ ទិន្នន័យការលក់រាយ (Retail Sales) បានស្ទុះឡើងវិញបន្តិច បន្ទាប់ពីធ្លាក់ចុះមុននេះ បង្ហាញពីតម្រូវការអ្នកប្រើប្រាស់នៅតែមានស្ថេរភាព។ ទោះជាយ៉ាងណា ទិន្នន័យ Initial Jobless Claims បានកើនលើសការរំពឹងទុក បង្ហាញពីការធ្លាក់ចុះបន្តិចនៃទីផ្សារការងារ។

សរុបមក ទិន្នន័យទាំងនេះគាំទ្រការរំពឹងថា ធនាគារកណ្តាលអាមេរិកអាចរក្សាអត្រាការប្រាក់ក្នុងកម្រិតខ្ពស់រយៈពេលវែង។

| English Version |

Weekly Data Summary Report

As of May 18, 2026

Below is a summary of the United States, primarily based on critical events related to President Donald Trump, economic data releases, and geopolitical conflicts from the last week.

Disclaimer: Please note this is opinion-based; do not take it as investment advice.

Key Highlight Events:

U.S.-Iran War: Over the past week, hopes for a potential peace deal between the U.S. and Iran have weakened. The U.S. initially proposed a deal, to which Iran responded with a counterproposal—later described as “garbage” by President Trump. Additionally, on May 18, 2026, President Donald Trump posted on Truth Social: “For Iran, the clock is ticking, and they better get moving, FAST, or there won’t be anything left of them. TIME IS OF THE ESSENCE! President DJT.”

Overall, tensions appear to be rising and could escalate further. In response to these developments, both WTI Crude Oil and Brent Oil CFDs recorded modest price increases last week amid heightened geopolitical uncertainty.

U.S.-China Summit: President Trump met with President Xi Jinping last week for the U.S.–China summit, which was also attended by several high-profile CEOs from both countries, including Elon Musk (Tesla), Jensen Huang (Nvidia), and Lei Jun (Xiaomi). While both sides described the discussions as productive, there were no major agreements on key issues such as tariffs, a trade truce extension, etc.

Despite the lack of concrete outcomes, overall relations appear to have improved, with tensions easing slightly. President Xi is also expected to visit the White House in the fall for a follow-up summit. Gold prices declined modestly over the past week, likely reflecting reduced safe-haven demand.

Kevin Warsh Appointed New Fed Chair: Last week marked the official confirmation of Kevin Warsh as the new Fed chair.

The Federal Reserve has maintained relatively high interest rates, with the possibility of further tightening. It remains uncertain whether Warsh’s appointment will shift the Fed’s policy direction. If interest rates rise, gold prices may face downward pressure due to a stronger U.S. dollar. Conversely, if rates are cut, gold prices may increase as the dollar weakens. However, in the near term, the most likely scenario is that rates remain unchanged.

Key U.S. Economic Data Release:

The latest U.S. data shows a mixed but slightly inflationary picture. CPI held steady month-on-month and rose to 3.8% year-on-year, while Core CPI came in above expectations, pointing to ongoing price pressures. PPI also surprised to the upside, reinforcing signs of persistent inflation. On the growth side, Retail Sales showed a modest rebound following the previous decline, suggesting stable consumer demand. However, Initial Jobless Claims rose above forecasts, indicating slight softening in the labor market. Overall, the data supports expectations that the Federal Reserve may keep interest rates higher for longer.