របាយការណ៍ទីផ្សារប្រចាំសប្តាហ៍ទស្សនវិស័យទីផ្សារប្រចាំសប្តាហ៍គិតត្រឹមថ្ងៃទី 23 ខែមិថុនា ឆ្នាំ 2026

កត្តាសំខាន់ៗដែលត្រូវតាមដានបំផុតសម្រាប់សប្តាហ៍នេះគឺនឹងដាក់បញ្ចូលនៅក្នុងរបាយការណ៍ខាងក្រោមនេះដោយវិនិយោគិនអាចប្រើប្រាស់ព័ត៌មានខាងក្រោមជាមូលដ្ឋានគ្រឹះមុនពេលធ្វើការសម្រេចចិត្តលើការជួញដូរលើទ្រព្យណាមួយ។ របាយការណ៍នេះរួមបញ្ចូលទាំងការវិភាគបែបសេដ្ឋកិច្ច (Fundamental Analysis) ដែលជាកត្តាសំខាន់ៗជំរុញចលនាទីផ្សារ និងការវិភាគបែបបច្ចេកទេស (Technical Analysis) រួមទាំងចលនាតម្លៃ និងតំបន់សាច់ប្រាក់ (Liquidity Zones) សំខាន់ៗ ដែលវិនិយោគិនគួរតែតាមដាន។

ការបដិសេធ (Disclaimer): របាយការណ៍នេះធ្វើឡើងក្នុងគោលបំណងផ្សព្វផ្សាយការអប់រំ និងព័ត៌មានដែលគួរដឹងតែប៉ុណ្ណោះ។ សូមមេត្តាកំុប្រើប្រាស់របាយការណ៍នេះជាដំបូន្មានវិនិយោគ ឬជាសញ្ញាសម្រាប់ការជួញដូររបស់អ្នក។

ការវិភាគបែបសេដ្ឋកិច្ច (Fundamental Analysis)

កត្តាបីយ៉ាងដែលត្រូវផ្តោតលើសប្តាហ៍នេះ៖

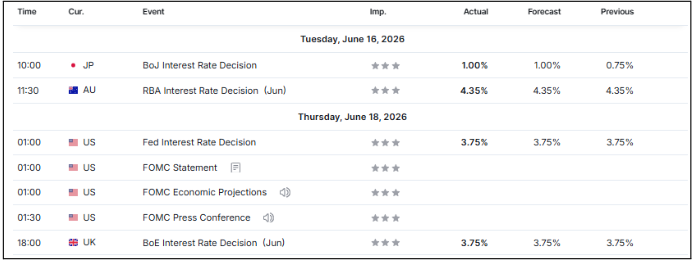

ព្រឹត្តិការណ៍សេដ្ឋកិច្ចសំខាន់ៗកាលពីសប្តាហ៍មុន – ផ្តោតលើកិច្ចប្រជុំធនាគារកណ្តាលអាមេរិក (FOMC Meeting)

សប្តាហ៍កន្លងមក ប្រតិទិនសេដ្ឋកិច្ចបានផ្តោតសំខាន់ទៅលើការសម្រេចអត្រាការប្រាក់របស់ធនាគារកណ្ដាលធំៗ។ ធនាគារកណ្ដាលទាំងនោះរួមមាន ជប៉ុន អូស្ត្រាលី អង់គ្លេស និងសំខាន់បំផុត គឺសហរដ្ឋអាមេរិក។

ធនាគារកណ្ដាលធំៗទាំងអស់បានសម្រេចអត្រាការប្រាក់ស្របតាមការរំពឹងទុក។ ខណៈដែលធនាគារកណ្ដាលអូស្ត្រាលី (RBA) និងធនាគារកណ្ដាលអង់គ្លេស (BoE) បានរក្សាអត្រាការប្រាក់ដដែល ធនាគារកណ្ដាលជប៉ុន (BoJ) បានបង្កើនអត្រាការប្រាក់ 0.25%។

ជាទូទៅ ការឡើងអត្រាការប្រាក់តែងតែជួយពង្រឹងរូបិយប័ណ្ណ ប៉ុន្តែការឡើងនេះមិនបានជួយឲ្យប្រាក់យ៉េនជប៉ុន (JPY) ខ្លាំងឡើងទេ។ គូរូបិយប័ណ្ណ USDJPY នៅតែស្ថិតនៅកម្រិតប្រហែល 160 ដោយសារតែភាពខុសគ្នាអត្រាការប្រាក់រវាងសហរដ្ឋអាមេរិក និងជប៉ុននៅតែធំខ្លាំង។

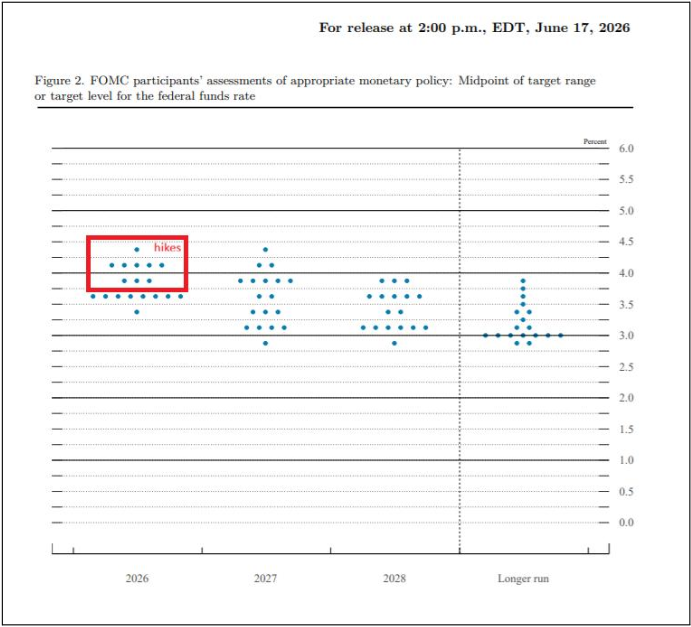

ចំពោះដុល្លារអាមេរិក (USD) ធនាគារកណ្ដាលអាមេរិក (Fed) បានសម្រេចរក្សាអត្រាការប្រាក់ដដែល។ ទោះជាយ៉ាងណា Fed បានបង្ហាញគោលជំហរតឹងតែងសម្រាប់គោលនយោបាយរូបិយវត្ថុ (hawkish tone)។

Dot plot ចុងក្រោយបង្ហាញការចែកចាយទស្សនៈដែលមានភាព hawkish គួរឱ្យកត់សម្គាល់។ ក្នុងចំណោមមន្ត្រី 18 នាក់ដែលបានដាក់ការព្យាករណ៍ មាន 9 នាក់រំពឹងថានឹងមិនមានការកាត់អត្រាការប្រាក់មុនដាច់ឆ្នាំ, 8 នាក់រំពឹងថាអត្រាការប្រាក់នឹងនៅដដែល ហើយមានតែ 1 នាក់ប៉ុណ្ណោះដែលរំពឹងថានឹងមានការកាត់អត្រាការប្រាក់។

គិតត្រឹមថ្ងៃទី 22 មិថុនា 2025 ម៉ោង 1:47 រសៀល (GMT+7) មាសបានធ្លាក់ចុះ 4.05% ចាប់តាំងពីកិច្ចប្រជុំ FOMC ដោយសារទីផ្សារបានវាយតម្លៃឡើងវិញអំពីការរំពឹងទុកអត្រាការប្រាក់។

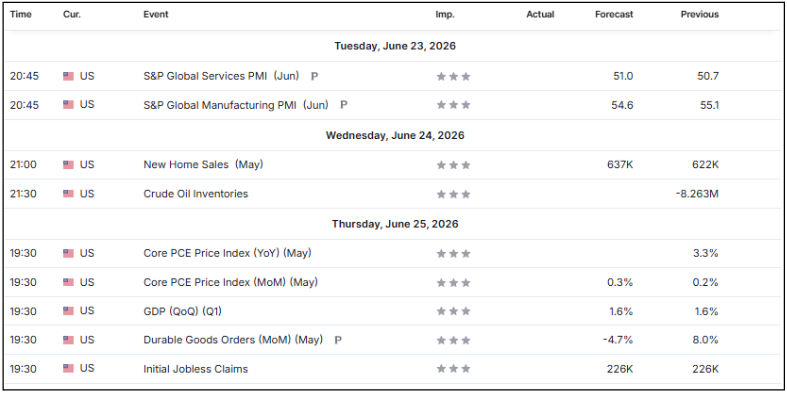

ព្រឹត្តិការណ៍ប្រតិទិនសេដ្ឋកិច្ចសប្តាហ៍នេះ

បន្ទាប់ពីកិច្ចប្រជុំ FOMC សប្តាហ៍មុន ដែលធនាគារកណ្ដាលអាមេរិកបានរក្សាអត្រាការប្រាក់ ប៉ុន្តែបានបង្ហាញទស្សនៈ hawkish តាមរយៈការព្យាករណ៍ និងសេចក្តីអធិប្បាយ សប្តាហ៍នេះទិន្នន័យសេដ្ឋកិច្ចនឹងត្រូវបានតាមដានយ៉ាងជិតស្និទ្ធ ដើម្បីបញ្ជាក់ថាតើសេដ្ឋកិច្ចអាមេរិកនៅតែរឹងមាំគ្រប់គ្រាន់ដើម្បីគាំទ្រការរក្សាអត្រាប្រាក់នៅកម្រិតខ្ពស់កាន់តែយូរ។

ទិន្នន័យសំខាន់ៗរួមមាន៖ សន្ទស្សន៍អ្នកគ្រប់គ្រងការទិញផលិតកម្មរបស់ S&P (S&P Global Manufacturing PMI) និង សន្ទស្សន៍អ្នកគ្រប់គ្រងការទិញសេវាកម្មរបស់ S&P (S&P Global Services PMI) នៅថ្ងៃអង្គារ ការលក់ផ្ទះថ្មី (New Home Sales) នៅថ្ងៃពុធ, និងរបាយការណ៍សំខាន់ៗនៅថ្ងៃព្រហស្បតិ៍ រួមមានសន្ទស្សន៍ការចំណាយលើការប្រើប្រាស់ផ្ទាល់ខ្លួនស្នូល (Core PCE Price Index) ផលិតផលក្នុងស្រុកសរុបត្រីមាសទី 1 (GDP QoQ Q1) និង ការទាមទារគ្មានការងារធ្វើដំបូង (Initial Jobless Claims)។

សេណារីយ៉ូសំខាន់ៗដែលត្រូវតាមដាន៖

- សេណារីយ៉ូ hawkish ចំពោះ Fed: PMI បង្ហាញសកម្មភាពសេដ្ឋកិច្ចខ្លាំងជាងការរំពឹងទុក Core PCE លើសការព្យាករណ៍ GDP ត្រូវបានកែឡើងខ្ពស់ និង Initial Jobless Claims នៅកម្រិតទាប។ នេះនឹងពង្រឹងទស្សនៈ របស់ Fed ដោយគាំទ្រដុល្លារអាមេរិក ការរក្សាអត្រាប្រាក់នៅកម្រិតខ្ពស់កាន់តែយូរ និងទិន្នផលប័ណ្ណរដ្ឋ (Treasury yields) ខណៈអាចបង្កសម្ពាធលើតម្លៃមាស។

- លទ្ធផលអព្យាក្រឹត: PMI, Core PCE, GDP និង Jobless Claims ស្របតាមការរំពឹងទុក។ ក្នុងសេណារីយ៉ូនេះ ទីផ្សារអាចបន្តរក្សាការរំពឹងទុកបច្ចុប្បន្នចំពោះគោលនយោបាយ Fed ដោយមាសនៅតែអាស្រ័យលើកត្តាភូមិសាស្ត្រនយោបាយ។

- សេណារីយ៉ូ dovish ចំពោះ Fed: PMI បង្ហាញការថយចុះសកម្មភាពសេដ្ឋកិច្ច, Core PCE ទាបជាងការរំពឹងទុក, GDP ត្រូវបានកែចុះទាប, និង Jobless Claims កើនឡើង។ នេះអាចធ្វើឲ្យទីផ្សារសង្ស័យអំពីទស្សនៈ hawkish របស់ Fed និងបង្កើនការរំពឹងទុកការកាត់អត្រាការប្រាក់ នាំឲ្យដុល្លារធ្លាក់ និងគាំទ្រតម្លៃមាស។

ការយកចិត្តទុកដាក់ពិសេសនឹងផ្តោតលើការចេញផ្សាយ Core PCE Price Index នៅថ្ងៃព្រហស្បតិ៍ ដែលជារង្វាស់អតិផរណាដែល Fed ចូលចិត្តប្រើប្រាស់។ រាល់ភាពភ្ញាក់ផ្អើលក្នុងទិន្នន័យនេះអាចបង្កឲ្យមានការប្រែប្រួលខ្លាំងនៅក្នុងទីផ្សារមាស និងដុល្លារអាមេរិក។

ការចរចារវាងសហរដ្ឋអាមេរិក និងអ៊ីរ៉ង់នៅស្វីស៖ អ្វីដែលវិនិយោគិនមាសគួរតាមដាន

ការវិវត្តន៍ភូមិសាស្ត្រនយោបាយនៅតែជាកត្តាសំខាន់សម្រាប់ទីផ្សារហិរញ្ញវត្ថុ បន្ទាប់ពីមានកិច្ចចរចារវាងសហរដ្ឋអាមេរិក និងអ៊ីរ៉ង់ជាច្រើនលើក។

សប្តាហ៍មុន ភាគីទាំងពីរបានរាយការណ៍ថាបានចុះហត្ថលេខាលើអនុស្សរណៈនៃការយោគយល់ចំពោះបទឈប់បាញ់ (MoU) តាមប្រព័ន្ធអេឡិចត្រូនិក ដោយកំណត់គ្រោងការឈប់បាញ់រយៈពេល 60 ថ្ងៃ និងមានគម្រោងចុះហត្ថលេខាផ្លូវការនៅស្វីសនៅថ្ងៃសុក្រ។ ទោះជាយ៉ាងណា សាធារណៈជននៅតែមានការសង្ស័យអំពីភាពរឹងមាំនៃកិច្ចព្រមព្រៀង ខណៈអ៊ីស្រាអែលនៅតែបន្តប្រតិបត្តិការយោធានៅលីបង់។

ប៉ុន្តែពេលដល់ថ្ងៃសុក្រ ព្រឹត្តិការណ៍ចុះហត្ថលេខាបានត្រូវពន្យារពេល បន្ទាប់ពីអនុប្រធានាធិបតីអាមេរិក លោក JD Vance បានពន្យារពេលដំណើរទៅស្វីស។ មន្ត្រីអាមេរិកបានបញ្ជាក់ថា ដោយសារ MoU បានចុះហត្ថលេខារួចហើយ ការពិភាក្សានឹងផ្តោតលើការបញ្ចប់លម្អិត និងការអនុវត្តកិច្ចព្រមព្រៀង។

មកដល់ថ្ងៃនេះ អ្នកចរចាពីភាគីទាំងពីរបានបញ្ចប់ជុំដំបូងនៃការពិភាក្សានៅស្វីស ហើយបច្ចុប្បន្នកំពុងធ្វើការតាមផែនការ 60 ថ្ងៃ ដើម្បីឈានទៅកិច្ចព្រមព្រៀងពេញលេញ។

បញ្ហាសំខាន់មួយក្នុងការចរចានៅតែជាស្ថានភាពនៃច្រកសមុទ្រ Hormuz។ ខណៈកិច្ចព្រមព្រៀងដំបូងបានបង្កក្តីសង្ឃឹមថាផ្លូវដឹកជញ្ជូនសមុទ្រនឹងត្រូវបើកឡើងវិញ អ៊ីរ៉ង់ក៏បានសម្រេចបិទច្រកនេះវិញ ដោយអះអាងថាសហរដ្ឋអាមេរិកមិនបានគោរពការសន្យាក្នុងការទប់ស្កាត់ការវាយប្រហាររបស់អ៊ីស្រាអែលនៅលីបង់។

សេណារីយ៉ូសំខាន់ៗដែលត្រូវតាមដាន៖

- សេណារីយ៉ូ bullish សម្រាប់មាស: សហរដ្ឋអាមេរិក និងអ៊ីរ៉ង់មានវឌ្ឍនភាពឆ្ពោះទៅកិច្ចព្រមព្រៀងពេញលេញ និងច្រកសមុទ្រ Hormuz ត្រូវបានបើកឡើងវិញ។ តម្លៃប្រេងធ្លាក់ អាចបន្ថយសម្ពាធអតិផរណា បង្កើនការរំពឹងទុកការកាត់អត្រាការប្រាក់របស់ Fed ដែលគាំទ្រតម្លៃមាស។

- សេណារីយ៉ូ bearish សម្រាប់មាស: ការចរចារជាប់គាំង ភាពតានតឹងកើនឡើង ឬច្រកសមុទ្រ Hormuz នៅតែត្រូវបានបិទ។ នេះអាចធ្វើឲ្យតម្លៃប្រេង និងអតិផរណានៅខ្ពស់ ជំរុញ Fed ឲ្យរក្សាអត្រាការប្រាក់ខ្ពស់យូរ ដែលជាទូទៅបង្កសម្ពាធលើមាស។

- លទ្ធផលអព្យាក្រឹត: ការចរចាបន្តទៅមុខដោយគ្មានការរីកចម្រើន ឬដួលរលំធំ។ ក្នុងសេណារីយ៉ូនេះ តម្លៃមាសប្រហែលមានបម្រែបម្រួលតិចតួច។

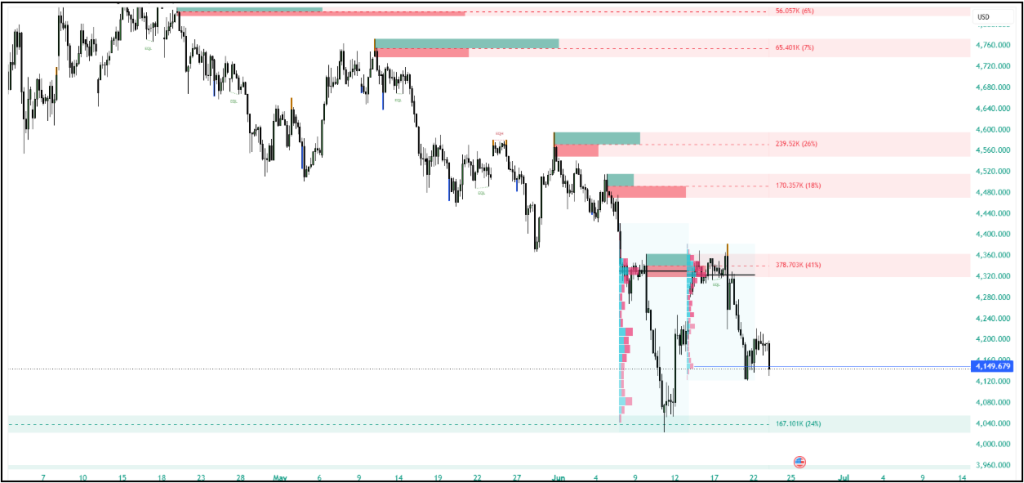

ការវិភាគបច្ចេកទេស (Technical Analysis)

សេណារីយ៉ូសំខាន់ៗដែលត្រូវតាមដានរួមមាន៖

- និន្នាការបច្ចុប្បន្ន៖ បច្ចុប្បន្នទីផ្សារស្ថិតនៅក្នុងទិសដៅចុះ នៅដំណាក់កាលចុងSwing ប្រចាំខែព្រោះជាសប្តាហ៍ទី៤នៃខែ។

- កម្រិត (Support Level)៖ ថ្មីៗនេះតម្លៃបានជួបប្រទះនឹងការរុញច្រានត្រឡប់ឡើង មកវិញនៅជុំវិញកម្រិត 4040 ដុល្លារ។

- កម្រិតសំខាន់៖ ប្រសិនបើតម្លៃនៅតែបន្តជួញដូរនៅលើងតម្លៃ 4040 ដុល្លារ នោះសន្ទុះនៃការឡើងត្រឡប់ទៅលើវិញក្នុងរយះពេលខ្លីនៅតែខ្លាំងហើយអាចត្រឡប់ទៅរកតម្លៃ 4320វិញ។

- ទិដ្ឋភាពយុទ្ធសាស្ត្រ៖ សម្រាប់អ្នក Swing Short អាចសម្រាកបានក្នុងសប្តាហ៍នេះរង់ចាំឱកាសនៅសប្តាហ៍ទី១នៃខែបន្ទាប់ នៅបន្ទាប់ពី ទិន្នន័យ Non Farm Employment Change ចេញមក។

| English Version |

This report highlights key developments for the week ahead, providing investors with relevant context to support informed trading decisions. It covers both fundamental analysis—the primary drivers behind market movements—and technical analysis, including price action and key liquidity zones that traders should monitor.

Disclaimer: This material is provided for educational and informational purposes only and should not be considered as investment advice or a trading signal.

Fundamental Analysis

Three factors to focus on this week from the fundamental side:

Last Week’s Economic Calendar Events – FOMC Meeting in Focus

Last week’s economic calendar was heavily focused on major central banks’ interest rate decisions. Those major central banks include Japan, Australia, England, and most importantly, the US. All central banks ended up with the forecasted interest rate. While the Reserve Bank of Australia (RBA) and the Bank of England (BoE) held their interest rates, the Bank of Japan (BoJ) actually increased its interest rate by 0.25%. While a rate hike normally strengthens the currency, this rate hike did little to strengthen the Japanese Yen (JPY). The USDJPY pair is still sitting at the 160 level despite the rate hike, mainly due to the fact that there is still a big interest rate discrepancy between the USD and JPY.

As for the USD, the Fed decided to hold interest rates. However, the Fed presented hawkish tones.

The latest dot plot showed a relatively hawkish distribution of expectations. Of the 18 officials who submitted projections, nine anticipated at least one rate hike before year-end, while eight expected rates to remain unchanged and only one projected a rate cut.

As of June 22, 2025 1:47 PM (GMT+7), gold has declined 4.05% since the FOMC meeting, as markets reassessed interest rate expectations.

This Week’s Economic Calendar Events

Following last week’s FOMC meeting, where the Federal Reserve maintained interest rates but signaled a relatively hawkish outlook through its projections and commentary, this week’s economic data will be closely watched for confirmation of whether the U.S. economy remains strong enough to support a higher-for-longer interest rate environment.

The key releases include S&P Global Manufacturing and Services PMI data on Tuesday, New Home Sales on Wednesday, and a series of high-impact reports on Thursday, including the Core PCE Price Index, Q1 GDP, Durable Goods Orders, and Initial Jobless Claims.

Key scenarios to watch include:

- More hawkish for the Fed: S&P Global PMI surveys show stronger-than-expected business activity, Core PCE inflation exceeds forecasts, Q1 GDP is revised higher, and Initial Jobless Claims remain low. This would reinforce the Fed’s higher-for-longer stance, supporting the U.S. dollar and Treasury yields while creating potential headwinds for gold prices.

- Neutral outcome: S&P Global PMI, Core PCE, GDP, and Initial Jobless Claims broadly match market expectations. In this scenario, investors may maintain current expectations for the Fed’s policy path, with gold likely remaining sensitive to geopolitical developments.

- More dovish for the Fed: S&P Global PMI surveys indicate slowing business activity, Core PCE inflation comes in below expectations, GDP growth is revised lower, and Initial Jobless Claims rise. Such results could lead investors to question the Fed’s hawkish outlook and increase expectations for future rate cuts, potentially weighing on the U.S. dollar and providing support for gold prices.

Particular attention will be paid to Thursday’s Core PCE Price Index release, the Fed’s preferred measure of inflation. As markets continue to assess whether inflation is moving sustainably toward the Fed’s target, any surprise in the data could trigger significant moves across gold and the U.S. dollar.

US-Iran Talks in Switzerland: What Gold Investors Should Watch

Geopolitical developments remain a key theme for financial markets following a series of negotiations between the United States and Iran.

Last week, both sides reportedly signed a Memorandum of Understanding (MoU) electronically outlining a 60-day ceasefire framework, with plans for an official signing ceremony in Switzerland. However, questions over the durability of the agreement emerged as Israel continued military operations in Lebanon despite the ceasefire framework. Iran has previously indicated that any agreement with the United States should also contribute to ending hostilities involving Israel and Lebanon.

The planned signing ceremony was subsequently delayed after U.S. Vice President JD Vance postponed his trip to Switzerland. U.S. officials stated that, since the MoU had already been signed electronically, discussions would focus on finalizing the details and implementation of the agreement.

Negotiators from both countries have since completed an initial round of discussions in Switzerland, with both sides now working within a 60-day roadmap aimed at reaching a comprehensive agreement.

A key issue for the negotiations remains the status of the Strait of Hormuz. While the agreement initially raised hopes that maritime trade routes would remain open, Iran later signaled renewed restrictions, arguing that the United States had failed to uphold its commitment to prevent further Israeli attacks in Lebanon.

Technical Analysis

Key scenarios to watch include:

- Current Trend: The market is currently in a downtrend, situated at the late stage of the monthly swing since it is the fourth week of the month.

- Support Level: Recently, the price has experienced an upward rejection (bounce) around the $4040 level.

- Key Level: If the price continues to trade above $4040, the short-term bullish momentum remains strong, and the price could potentially return to the $4320 level.

- Strategic Outlook: For swing short traders, it is best to take a break this week and wait for a new opportunity in the first week of next month, after the release of the Non-Farm Employment Change data.